If you want to understand the shifting tectonic plates of the global economy, you could read the latest policy white papers out of Washington, or you could simply look at the photograph of Friedrich Merz in Hangzhou.

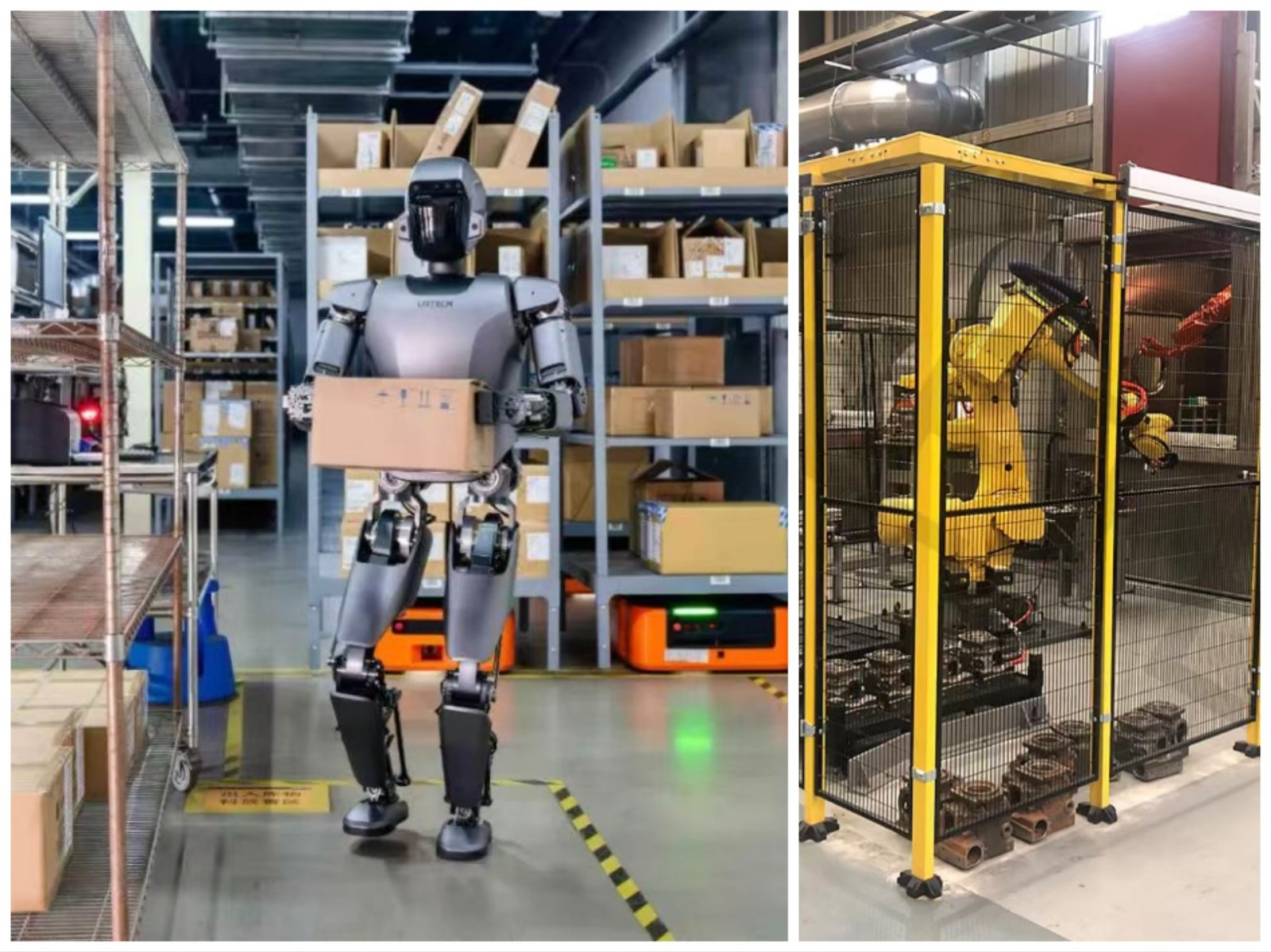

There stood the German Chancellor—a politician whose brand is practically forged from stern Atlanticist rigour and conservative economic prudence—in a brightly lit showroom, watching humanoid robots execute fluid Kung Fu routines and dance alongside a choreographed troupe of mechanical, quadruped dogs. The company playing host was Unitree Robotics, a vanguard of China’s booming embodied artificial intelligence sector.

For a Western leader whose closest allies have spent the better part of three years speaking feverishly of “de-risking” and erecting high fences around critical technologies, the optics were arresting. It looked, to the untrained eye, like a spectacular geopolitical gaffe. But look closer, and Mr Merz’s visit was anything but accidental. It was a stark, calculated signal that in the high-stakes realm of advanced manufacturing, the era of blunt de-coupling is dead.

“Strategic re-coupling has arrived.”

To understand why the undisputed powerhouse of European industry is quietly plugging its economy back into the “Robot Belt”—the vast, hyper-innovative south-eastern industrial corridor stretching from Guangdong up through Zhejiang, Jiangsu, and Shanghai—one must confront the increasingly sclerotic state of Germany’s own factories.

A decade ago, the German vision of Industrie 4.0 was the envy of the world. It was conceived as a marvel of precision engineering and highly structured automation. Today, however, that same system is increasingly bedevilled by punishing capital costs, rigid legacy software, and sluggish iteration cycles. The existential dread is most palpable in the legendary German automotive sector. As legacy marques watch agile Chinese electric vehicle (EV) brands aggressively capture market share—dominating everything from the European mainland to the lucrative right-hand-drive strongholds of the Commonwealth—a chilling realisation has dawned in Stuttgart and Munich: traditional engineering excellence is no longer enough to win the global technology race.

China, meanwhile, has fundamentally rewritten the rules of hardware. It has transformed its manufacturing heartlands into unparalleled global hubs for agile iteration. Firms like Unitree are driving down the cost of highly complex components, such as high-torque actuators, joint motors, and advanced LiDAR sensors, with a speed that leaves Western competitors gasping.

Where traditional German industrial robots are magnificent but caged beasts—designed to perform single, repetitive tasks in highly structured, heavily guarded environments—China’s new breed of embodied AI is entirely different. It is flexible, comparatively cheap, and uniquely capable of navigating the unstructured, chaotic “brownfield” factory floors that dominate much of the Western industrial landscape.

For a middle power like Germany, severing these critical supply chains in the name of ideological purity is no longer viewed as a noble stand; it is viewed as an act of economic self-harm.

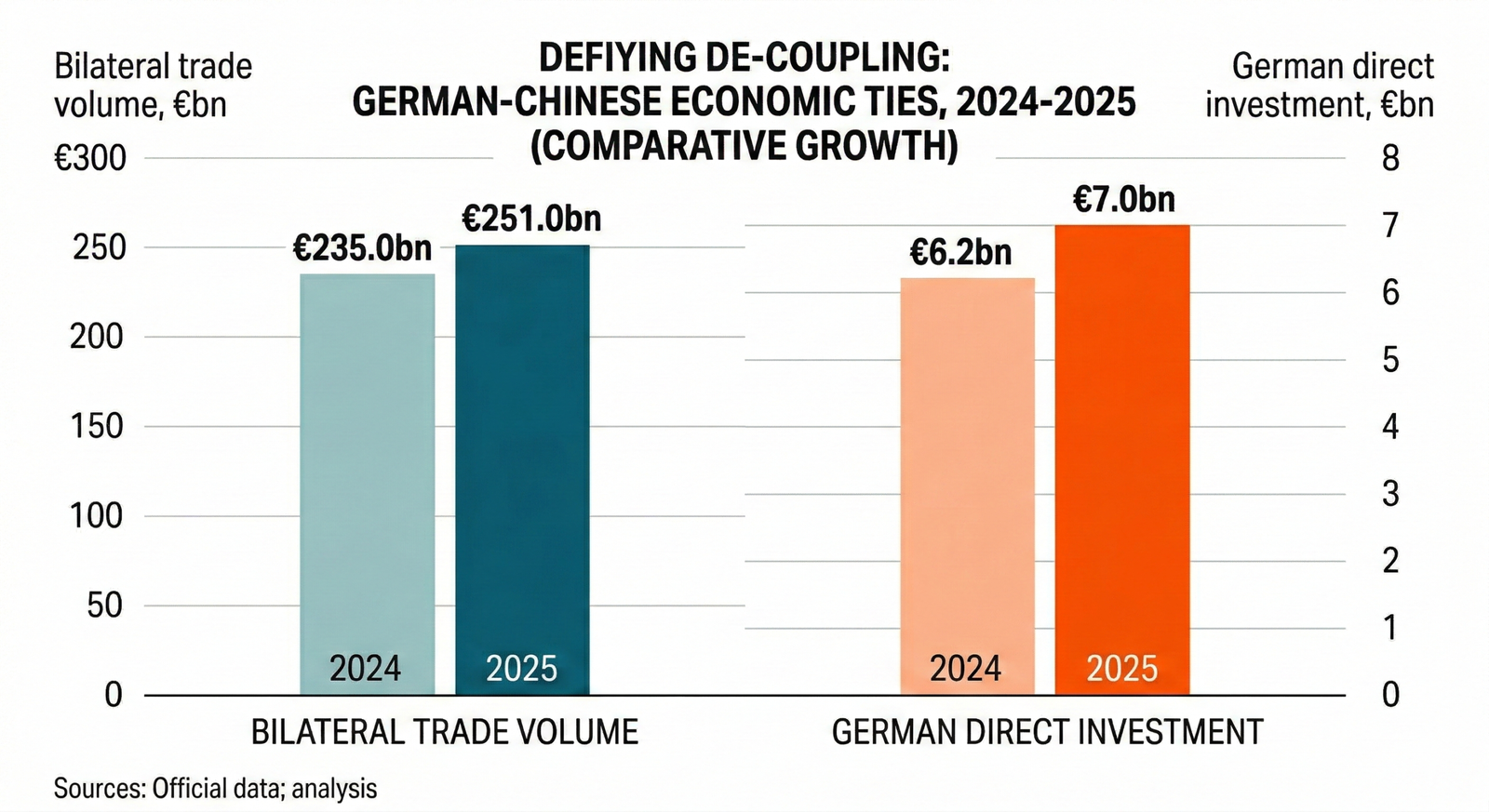

Mr Merz’s pragmatism is merely the public face of a quiet, overwhelming consensus in European boardrooms. The numbers tell a story that political rhetoric cannot obscure. Official data for 2025 confirmed that bilateral trade volumes between the two nations surpassed €251bn, with new German direct investment into China surging to roughly €7bn. Capital and industry are actively ignoring the political de-coupling narrative emanating from the United States.

Washington has long pressured its European allies to diversify away from Chinese supply chains, arguing that dependence on Beijing for foundational technologies poses an unacceptable national security risk. Yet, Berlin is charting a subtly divergent course, opting for a delicate, clear-eyed hedging strategy. It is choosing to manage, rather than sever, its interdependence with the world’s foremost manufacturing superpower.

Enter a framework akin to the “Carney model.” Championed by financial statesmen like Mark Carney, this approach advocates for strategic autonomy through diversified, sector-specific cooperation rather than blanket, zero-sum isolation.

Make no mistake: this is not a return to the naive, laissez-faire globalisation of the early 2000s, where Western firms traded intellectual property for market access with reckless abandon. This new paradigm is highly transactional, thoroughly unsentimental, and strictly ring-fenced.

In practice, this means German industrial titans will increasingly source modular intelligence from the Chinese supply chain. They will gladly purchase the hyper-advanced robotic limbs, the agile EV chassis architectures, and the AI-driven components perfected in Hangzhou and Shenzhen. They recognise that to build a factory of the future, they desperately need the hardware iteration speed that only the Robot Belt can currently provide.

However, they will keep a white-knuckled grip on the ultimate levers of control. Final system integration, proprietary factory network software, and localised data security will remain strictly in European hands. Furthermore, we are likely to see German firms actively partnering with Chinese start-ups to jointly draft the international safety and operating standards for humanoid robots—fusing Germany’s historical regulatory influence with China’s massive real-world deployment data.

It is a model of “co-opetition”, designed to marry German safety standards and legendary engineering reliability with Chinese artificial intelligence prowess and hardware scale. It allows Germany to modernise its ageing industrial base without surrendering the central nervous system of its manufacturing economy.

It is, undoubtedly, a delicate tightrope to walk. Hawks will warn of Trojan horses, and the diplomatic friction will be immense. Yet, as the mechanical Kung Fu displays in Hangzhou demonstrated so vividly, the geopolitical centre of gravity for agile automation has shifted permanently eastward. In the emerging multipolar order, durable prosperity depends less on rigidly choosing sides and more on mastering the complexities of the supply chain. For Germany, leveraging the next generation of global innovation is no longer a matter of opportunism; it is the bedrock of survival. Those who stubbornly refuse to re-couple strategically risk rusting away entirely.