The Mathematical Illusion of “Aiming Higher”: Why China’s Sub-5% Growth is a Structural Certainty

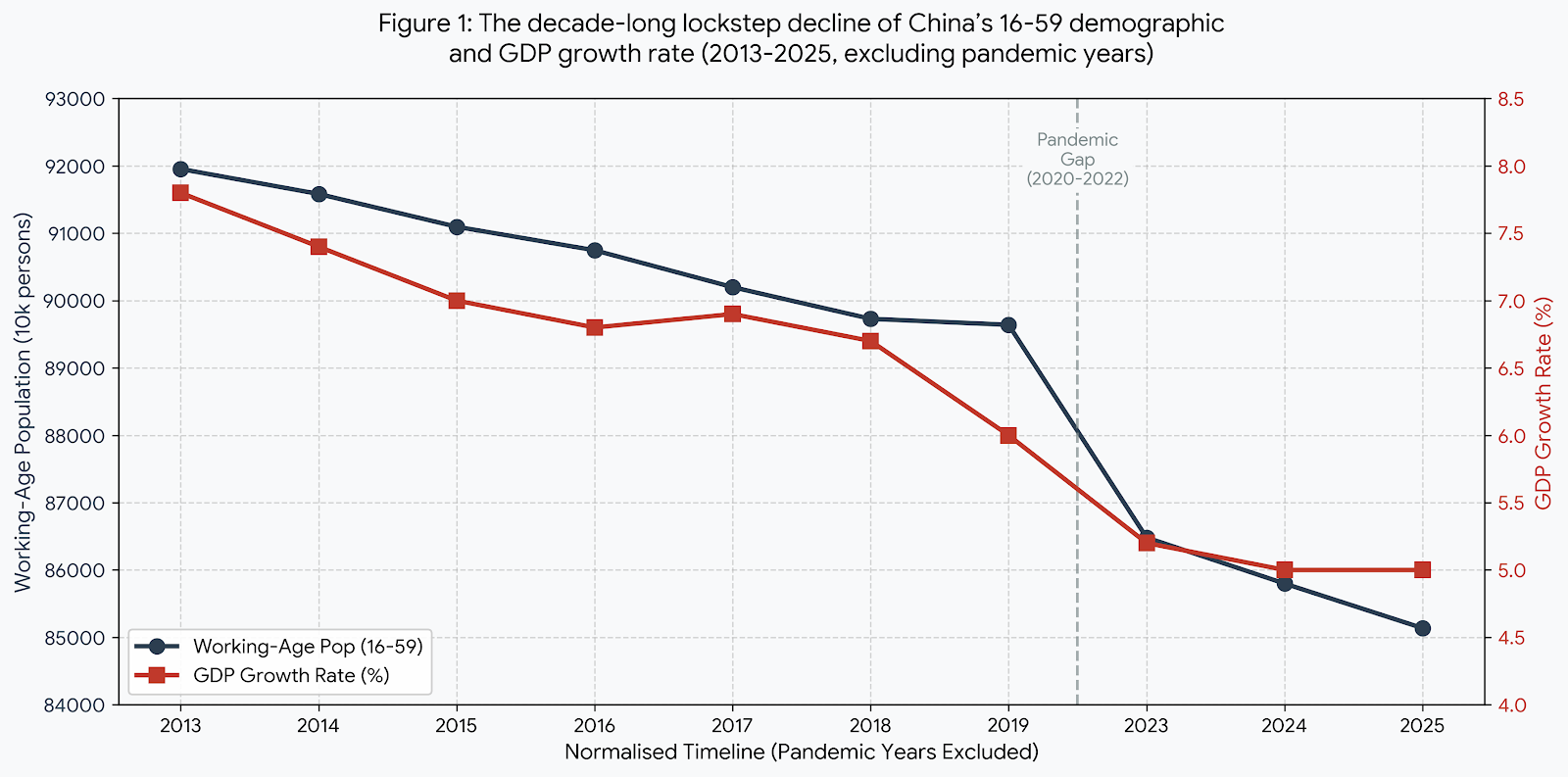

The Raw Data: A Decade of Normalised Growth (2013–2025)

To uncover the true underlying structural trend—the “grey rhino”—we must filter out the severe noise of the pandemic years (2020–2022). This leaves us with exactly 10 years of normalised economic operation.| Year | Working-Age Population (16-59) (10k persons) | GDP Growth Rate (%) |

|---|---|---|

| 2025 | 85,136 | 5.0 |

| 2024 | 85,798 | 5.0 |

| 2023 | 86,481 | 5.2 |

| 2019 | 89,640 | 6.0 |

| 2018 | 89,729 | 6.7 |

| 2017 | 90,199 | 6.9 |

| 2016 | 90,747 | 6.8 |

| 2015 | 91,096 | 7.0 |

| 2014 | 91,583 | 7.4 |

| 2013 | 91,954 | 7.8 |

(Source: National Bureau of Statistics of China.)

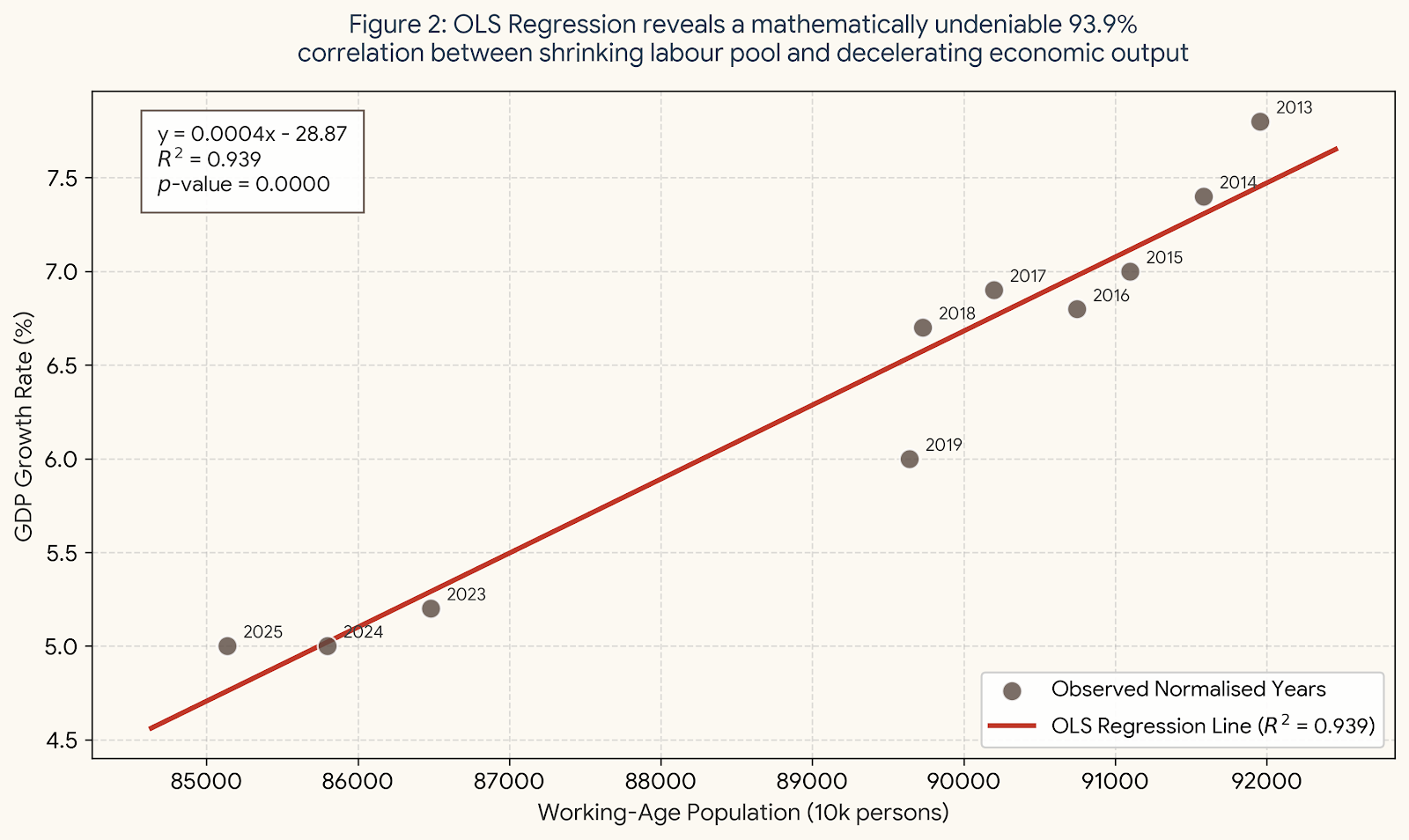

The Statistical Proof: The 93.9% Correlation

To prove that the decline in GDP growth is a structural inevitability rather than a lack of policy vigour, we apply a rigorous Pearson correlation and Ordinary Least Squares (OLS) regression analysis to the 10-year dataset above.1. The Pearson Correlation Coefficient ($r$)

Let $X$ represent the Working-Age Population and $Y$ represent the GDP Growth Rate. The formula is:

$$r=\frac{\sum(X_i-\bar{X})(Y_i-\bar{Y})}{\sqrt{\sum(X_i-\bar{X})^2\sum(Y_i-\bar{Y})^2}}$$

- Mean of $X$ ($\bar{X}$): 89,236.3

- Mean of $Y$ ($\bar{Y}$): 6.38

- Calculated $r$: 0.969

2. Ordinary Least Squares (OLS) Regression

To quantify the exact weight of this demographic drag, we calculate the OLS regression line ($Y=\alpha+\beta X$):- Slope ($\beta$): $\frac{\sum(X-\bar{X})(Y-\bar{Y})}{\sum(X-\bar{X})^2}\approx 0.0004$

- Intercept ($\alpha$): $\bar{Y}-\beta\bar{X}\approx -28.87$

$$\text{GDP Growth Rate}=-28.87+0.0004\times\text{Working-Age Population}$$

- R-squared ($R^2$): 0.939

- The Verdict: An astounding 93.9% of the variance in China’s slowing GDP growth over these normal operational years is explained by a single variable: the shrinking working-age population. The coefficient ($0.0004$) indicates that for every 10 million workers exiting the labour pool, the baseline macroeconomic growth potential drops by roughly 0.4 percentage points. You cannot legislate your way out of a disappearing workforce.

The Economic Theory Validation

This statistical phenomenon is perfectly anchored in classical macroeconomics.1. The Cobb-Douglas Production Function

The standard production function defines output ($Y$) based on Total Factor Productivity ($A$), Capital ($K$), and Labour ($L$):

$$Y=A\cdot K^\alpha\cdot L^{1-\alpha}$$

When converted into the Growth Accounting Equation:

$$\frac{\Delta Y}{Y}=\frac{\Delta A}{A}+\alpha\frac{\Delta K}{K}+(1-\alpha)\frac{\Delta L}{L}$$

Since 2013, the labour growth rate $\frac{\Delta L}{L}$ has been firmly negative. This mathematical term has shifted from being the primary engine of the Chinese economic miracle to a severe structural drag.

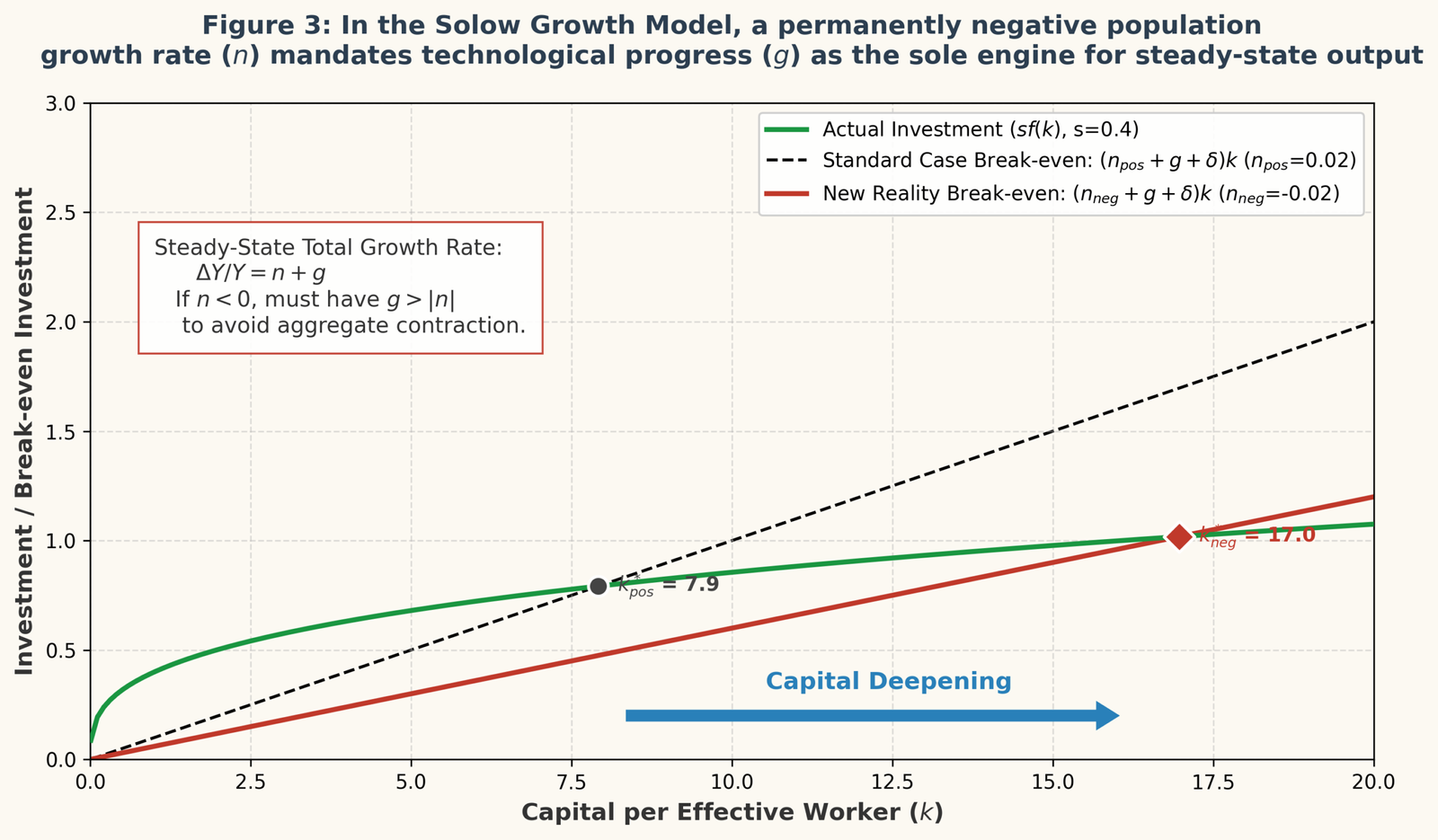

2. The Solow Growth Model

Looking at the Solow Model’s capital accumulation equation:

$$\Delta k=s f(k)-(n+\delta)k$$