VW will be bought by BYD, said Schularick. He’s wrong about the verb.

Moritz Schularick, president of the Kiel Institute for the World Economy, said Volkswagen would “likely be bought by a Chinese car maker like BYD.”

The press amplified it. Headlines ran with “buys” and “takes over.” A few editorial cartoonists went further, drawing BYD swallowing the VW badge whole. The imagery fed a familiar anxiety about German industrial decline.

All these verbs — Schularick’s “bought,” the headlines’ “takes over,” the cartoonists’ “eaten” — belong to the grammar of the last century. In the industrial age, a challenger proved its dominance by buying the incumbent. Geely bought Volvo from Ford in 2010. Tata bought Jaguar Land Rover two years earlier. That was how ascendancy was signalled. You wrote a cheque and raised your flag over someone else’s castle.

But BYD has no interest in VW’s castle. The castle is on fire.

The technology gap has inverted

Fifteen years ago, a Chinese automaker buying a European one was buying the future. Platforms, powertrains, safety engineering, brand equity. All of it flowed west to east.

That direction has reversed.

In the core EV stack, BYD needs nothing from Wolfsburg. Blade battery. 8-in-1 powertrain. DM 5.0 hybrid system. Its own electronic architecture. All self-iterating, all shipping at scale.

BYD’s vertical integration runs from lithium mines to semiconductor wafers to final assembly. The company even makes its own car lights and wiring harnesses. Roughly 75 percent of a BYD vehicle’s core components come from internal factories.

Volkswagen, meanwhile, had to invest approximately $700 million in XPeng in 2023 for a 4.99 percent stake. The purpose was not philanthropy. VW needed XPeng’s electronic architecture and smart cockpit software to fix its own roadmap. The student was buying tutoring from the classmate it once dismissed.

CARIAD, VW’s in-house software unit, tells the story in numbers. Founded in 2020 with a multi-year budget plan of 27 billion euros. By 2024, cumulative operating losses exceeded 5.8 billion euros. The ID.3, VW’s flagship electric hatchback, shipped late because the code would not hold. Ten thousand cars sat in tented lots in Zwickau, waiting for software patches delivered by technicians walking car to car with USB sticks. Six hours per vehicle. Three CEOs in three years.

This is not a company with technology BYD lacks. This is a company whose software division became a case study in how not to build a modern car.

What VW does still own is real. Chassis tuning. NVH discipline. Decades of European regulatory and crash-test knowledge. A network of test tracks and engineering centres that would take years to replicate. BYD’s DiSus intelligent body control system is closing the gap, but VW’s craft in ride and handling still carries genuine value.

The problem is that these are complements. They shorten timelines. They do not change trajectories.

The pension you would be buying

Here is where the arithmetic turns brutal.

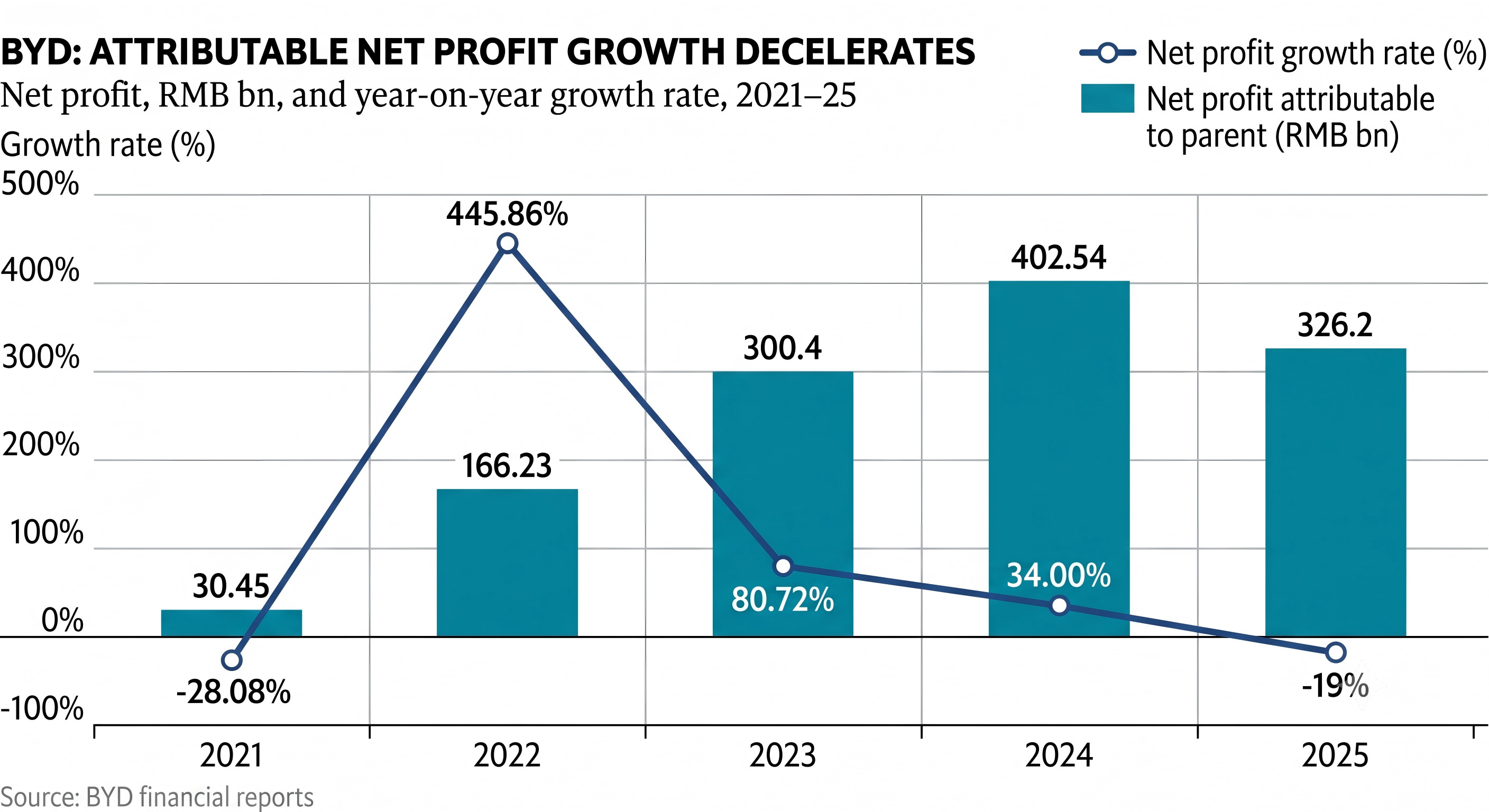

BYD’s 2025 net margin was 4.2 percent. Down from 5.35 percent the year before. Revenue reached 804 billion yuan. Net profit fell 19 percent to 32.6 billion yuan, squeezed by the most savage price war in automotive history. The company spent 63.4 billion yuan on research and development, nearly twice its net profit, because Wang Chuanfu treats R&D as savings rather than expenditure. Cash reserves stood at 167.8 billion yuan. Every yuan of that is spoken for. Factory build-outs in Hungary, Brazil, Thailand, Indonesia, Uzbekistan. A workforce of nearly 900,000. The tightrope is real.

Volkswagen carries a different kind of liability. European pension obligations. IG Metall, the metalworkers’ union that can veto strategy from Wolfsburg. Severance regimes where closing a single plant can cost billions of euros. A workforce whose benefits were negotiated in an era when VW was the most profitable automaker on earth.

The acquisition price would be the cheap part. The carrying cost is what kills you.

Picture the cash flow. BYD sells a Seal in Xi’an and pockets a thin margin. Somewhere in Lower Saxony, a retired VW line worker draws a pension that someone has to fund. Merge the two entities and the Xi’an margin flows west to the Wolfsburg pension. The vertical integration that makes BYD cheap becomes a pipe channelling money into a bottomless European obligation.

This is not strategy. It is a transfusion with no tourniquet.

The DNA incompatibility

This is the deepest problem, and the one that receives the least attention.

BYD’s vertical integration is not simply a matter of making a lot of things in-house. It is a closed ecosystem engineered for zero-latency iteration. Spec changes happen in days, not quarters. The company controls the battery chemistry, the chip design, the motor windings, the software stack, the body stamping. When a change is needed, there is no supplier to negotiate with. The conversation happens internally, often on the same campus.

VW is a classical assembler. Bosch, Continental, ZF, Magna define its boundaries. Changing a single feature in a VW vehicle means coordinating dozens of Tier 1 suppliers across multiple countries, each with its own contracts, tooling, and timelines. VW’s electronic architecture is a patchwork of supplier ECUs, each running its own code, updated on its own schedule.

CARIAD’s failure was not a management problem. It was structural. You cannot build integrated software on top of fragmented hardware. BYD figured this out years ago. VW is still learning it.

Imagine trying to run iOS on a Compaq from 1997. The hardware cannot accept the software. The assumptions are incompatible at the silicon level. That is what a BYD-VW merger would look like at the engineering layer.

And vertical integration has a dark side that makes this worse. It is a noose when utilisation drops. BYD can carry hundreds of factories and nearly 900,000 employees because it has millions of growing orders to feed them. The fixed costs are spread across a rising denominator. VW’s idle European plants, the very assets a merger would deliver, have a falling denominator. They would drag down BYD’s entire utilisation rate. The cost miracle depends on full factories. Idle factories are poison to the model.

VW would shatter the supply chain BYD spent thirty years building.

What taking over actually looks like

Schularick imagined a transaction. The press imagined a coronation. A new king walks into the old throne room and takes the seat.

That is not how power transfers in the electric era. Apple did not buy Nokia. Samsung did not acquire Motorola. They stood on a new technological track and watched the incumbents suffocate under their own accumulated complexity. Nokia still existed for years after it stopped mattering. Motorola’s name still appears on products. Existence and relevance are different conditions.

BYD is playing the same script. It does not need to own VW’s factories. It needs VW’s customers.

In China, that is already happening. VW’s once-dominant market share has been eroding for three years as BYD’s DM hybrid lineup and pure EV portfolio devour the price segments where VW built its volume. In Southeast Asia, Brazil, the Middle East, BYD is building the same moat with affordable plug-in hybrids and electric vehicles. BYD’s overseas revenue hit 311 billion yuan in 2025, up 40 percent year on year. VW’s home market is the last frontier.

There is a historical parallel worth noting. When Tesla needed a factory, it did not build one from scratch. It bought NUMMI, the former Toyota-General Motors joint venture plant in Fremont, California, at a fraction of its replacement cost. Toyota and GM had walked away. Tesla walked in.

VW’s idle plants in Europe may follow the same path. The Dresden Gläserne Manufaktur, once a showcase of German engineering pride, went dark recently. Not through acquisition of the company. Through distressed asset purchases. Through the quiet gravity of obsolescence.

The ten-million-unit horizon

Wang Chuanfu has spoken openly about a ten-million-unit annual sales target. Roughly where Toyota and VW sit today. The Schularick camp might argue that by then, BYD could afford VW.

Wrong. By then, it matters even less.

At ten million units, BYD’s own plants across Hungary, Brazil, Thailand, and Indonesia are running at capacity. VW’s internal combustion assets are not trophies by that point. They are depreciating liabilities on a balance sheet that nobody wants to inherit. Capital markets would punish, brutally, any decision to load a declining asset base onto a compounding one. Return on assets collapses. Return on equity follows. The thesis does not survive contact with a spreadsheet.

Wang Chuanfu said it at BYD’s 30th anniversary in late 2024. Daring to spend heavily on research and development is not burning money. It is saving money. The corollary he left unsaid: buying Volkswagen is adopting a hospital bill.

The verb that matters

Schularick said “bought.” The headlines said “takes over.” A few cartoonists said “eaten.” BYD is doing none of these.

What BYD is doing is closer to waiting. Letting VW age in its own system, under its own costs, with its own pension obligations and its own idle factories. Every quarter that passes, VW’s European assets depreciate a little more. Every quarter, BYD’s vertical integration deepens a little more.

VW will still exist in 2030. Probably 2040. The brand will persist. Some factories will run. But there is a difference between existing and mattering.

In Shenzhen, they are patient about the second one.